Recent global events have reinforced a theme that investors cannot ignore: higher energy prices are once again becoming a meaningful macroeconomic risk.

Oil prices have moved sharply higher in March, reflecting renewed concern around Middle East supply disruption and the ongoing closure of the Strait of Hormuz. For New Zealand, this matters. Higher fuel costs feed directly into transport, freight, airfares and imported inflation, while also weighing on household confidence and broader economic activity.

The Reserve Bank of New Zealand has acknowledged this challenge. The likely near-term outcome is a more difficult mix of softer growth and firmer headline inflation. In practical terms, that creates a market environment where selectivity becomes increasingly important.

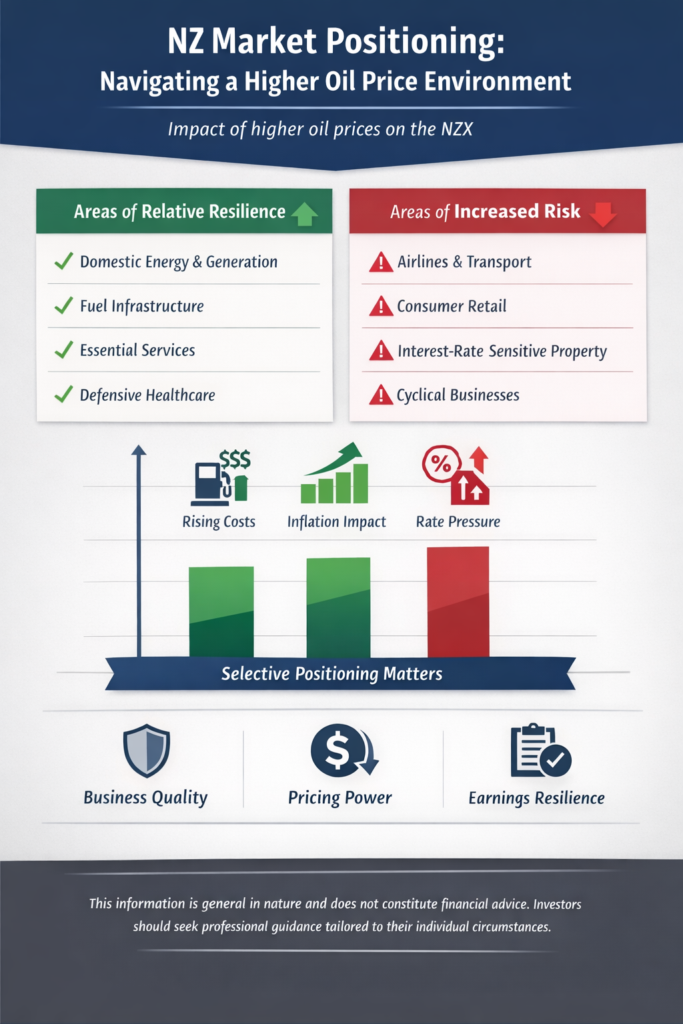

In our view, the NZX is unlikely to respond evenly to a prolonged oil shock. Some businesses are relatively well placed, particularly those tied to domestic energy security, essential infrastructure and defensive earnings. Others remain more exposed, especially where profitability is vulnerable to fuel costs, weaker consumer demand or higher-for-longer interest rates.

Areas of relative resilience

We continue to see merit in businesses linked to domestic energy generation, fuel infrastructure and essential services.

Channel Infrastructure remains well positioned given the strategic value of fuel import capacity and storage in a more fragile supply environment. The investment case is strengthened when energy security becomes more important.

Within utilities, Meridian Energy, Contact Energy and Genesis Energy all stand to benefit from increased investor focus on domestic generation and system resilience. These are not direct beneficiaries of higher oil prices in the traditional sense, but they do offer exposure to assets whose strategic importance rises as imported energy becomes more expensive and uncertain.

Defensive healthcare exposure also remains attractive. EBOS continues to stand out as a quality name with resilient earnings characteristics, while Fisher & Paykel Healthcare retains defensive appeal, even though it is not immune to freight and supply chain pressures.

We also see relative resilience in selected infrastructure and service businesses. Ports, telecommunications and other essential network assets are typically better placed than cyclical sectors when inflation and growth risks rise together.

Areas where caution remains warranted

Transport-exposed businesses remain more vulnerable in this environment. Air New Zealand is the clearest example, with higher fuel costs, pressure on discretionary travel demand and ongoing operational constraints all creating a more challenging earnings backdrop.

Freight and logistics businesses are more mixed. Quality operators such as Mainfreight and Freightways have strong franchises, but margins can still come under pressure when fuel, labour and economic growth all move in the wrong direction at once.

Property also requires caution. While some listed property and retirement names have improved operationally and strengthened balance sheets, the sector remains sensitive to bond yields, funding costs and valuation pressure. If higher oil prices delay the path to lower interest rates, these businesses may continue to face a tougher backdrop than the market had hoped for earlier in the year.

Consumer-facing cyclicals remain the most vulnerable part of the market. When fuel and living costs rise, discretionary spending typically comes under pressure. That creates a difficult environment for lower-margin retailers and businesses dependent on household confidence.

Our broad positioning view

If this oil shock proves temporary, market leadership could rotate again reasonably quickly. However, if higher energy prices persist, we believe the market is likely to continue favouring:

- Domestic energy and electricity generation

- Fuel infrastructure and strategic logistics assets

- Defensive healthcare and essential services

- Quality infrastructure with resilient cashflows

At the same time, we would remain more cautious on:

- Airlines and fuel-intensive transport

- Consumer discretionary retailers

- Higher-duration property exposures

- Businesses with weaker pricing power in a cost-driven slowdown

Final thoughts

This is not yet a crisis scenario, but it is a reminder that external shocks can quickly reshape market leadership.

For investors, the key is not to react emotionally to headline volatility, but to stay focused on business quality, pricing power, balance sheet strength and earnings resilience. Periods like this tend to reward disciplined portfolio construction and a clear understanding of which companies are exposed to the shock, and which may prove more durable through it.

In our view, that discipline is especially important now.